This is a four-part series on how early stage B2B software companies should approach product marketing. Part 1 is about the role of product marketing at the early stage, Part 2 describes a positioning framework I like to use, Part 3 describes my favorite formats for documenting positioning and Part 4 is a summary and commentary on the most effective frameworks I know for pricing and packaging.

I’ve found this framework incredibly useful for running a positioning exercise over the years. It’s inspired by April Dunford’s approach (highly recommend her book) and Clay Christensen’s jobs to be done framework (first described in the Innovator’s Solution).

Step 1 Start with the ‘jobs to be done’

What: Define the ‘jobs’ your product can be ‘hired’ to perform

Why: As Peter Drucker once said, customers don’t buy products or features, they buy benefits. Jobs-to-be-done helps you look at your product from your customers perspective, making it easier to separate the benefits from the features.

Example:

Take Cloudflare’s home page for example. They don’t mention a single product or feature, instead focusing on the benefits their target customers most care about — security, reliability, privacy and speed.

Benefit

Example products or features

Security

DDoS Protection, SSL/TLS

Reliability

CDN, Load Balancing

Speed

SSL/TLS

Privacy

CDN, DDoS Protection

Which customer jobs could have led them to identify these core benefits? Having not worked at Cloudflare, I can only speculate, but I imagine they could be something along the lines of:

I want to protect my internet assets from bad actors.

I want my web applications to deliver the best performance regardless of where my users are located.

I want user data to stay private and encrypted when it moves between my servers and user applications.

My applications should be able to handle drastic changes in traffic without changes in performance.

As an early stage company, you probably only have one or two products. The benefits you identify will be more granular than Cloudflare. This typically makes it harder to separate them from your features.

Step 2 Segment your TAM

What: Segment customers in your TAM using obvious and visible characteristics.

Why: For segmentation to be effective, it needs to be based on obvious and visible characteristics for a number of reasons –

They drive alignment across the team by helping engineering, sales and product unambiguously define different customer types in their TAM. There’s very little room for confusion when you use characteristics like ‘JavaScript developer’, ‘sales manager, ‘SDR’, ‘lead generation software provider’, ‘BPO’ etc.

Clearly defined and labeled customer segments make demand generation and prospecting easier down the line.

They make it easier to categorize customer feedback.

They also make it easier to identify and evaluate competitors.

Finally, they help you see which features are most used by customers with different characteristics, a critical input for packaging.

Let your understanding of the value provided by your product guide identifying these characteristics. They can be external — company size, number of seats, title or role or related to the product — usage or time to deploy the solution.

Example:

Gong.io does a fantastic job of segmenting their TAM using company roles and responsibilities.The product records sales conversations and uses AI to transcribe and analyze calls to derive insights that can improve sales performance. Insights include topics discussed, objections, competitors mentioned, spotting red flags and identifying opportunities for coaching.

They’ve adopted a broader position to start — ‘Revenue Intelligence’ vs ‘Sales Intelligence’, so that they can sell directly to the top decision maker on the sales side, whether that’s the CRO, COO or another executive title. It also positions them as a strategic investment as opposed to yet another sales acceleration tool.

But they’ve also done a great job targeting all of the other roles that could either be influencers or decision makers in buying the product with positioning that speaks specifically to their ‘jobs to be done’.

Step 3 Map jobs to be done to benefits

What: Map the ‘jobs’ each segment cares about to the benefits delivered by your product or feature.

Why: Each customer segment does not care about all the benefits you have to offer. Mapping helps you identify which products or features, and therefore benefits you highlight when positioning your product to a particular customer segment.

Example

Gong again does a great job here. They recognize that their product is valuable to any role responsible for sales performance like sales leaders, frontline sales managers, sales enablement managers and account executives.

Each role needs Gong for a different set of jobs:

Role

Jobs-to-be-done

Sales Leader

I need my sales team to be closing deals using a consistent and predictable process.

Sales Manager

I need all my reps to perform like my best reps.

Sales Enablement

I need new sales reps to become productive as fast as possible and onboarded sales reps to continue hitting their goals.

Account Executive

I need to consistently meet or exceed my quota.

Each role as a result cares about different benefits:

Role

Benefits

Sales Leader

Ensure reps are adhering to the pitch and best practicesAbility to quantify and benchmark rep performanceMeasure and monitor sales process performance

Sales Manager

Efficient call coachingIdentify best practices and areas of improvementShare best practices within the team

Sales Enablement

Identify areas of improvementMonitor training adoption in the fieldIdentify new competitors and objections

Account Executive

Close more deals faster

You can see this reflected in dedicated web pages for each role:

What: Analyze alternatives available to each customer segment for these jobs

Why: You can’t identify and articulate benefits in a vacuum. They need to be positioned against alternatives already available to the customer. Also remember that doing nothing, or using Excel or Email, or building from scratch in-house (in the case of API infrastructure) can always be an alternative. Knowing your strengths and weaknesses relative to alternatives helps you identify which benefits to emphasize in your positioning, which ones to downplay, and also helps with objection handling in sales conversations.

Having created the CDP category and become the leading company in the space, they’re explicitly contrasting CDPs (and by extension Segment) against CRMs by focusing on the relative advantages that matter to their target customers — companies looking to build better customer experiences.

Their positioning focuses on:

Eliminating data lock-in through open APIs and frameworks.

Flexibility to use the tech stack of your choice when building customer experiences (cough force.com cough).

Removing inter-departmental silos to place the customer first.

Note another advantage of this approach. CRMs are much older than CDPs. Segment’s target customers are extremely familiar with CRMs. Explicitly positioning against CRMs gives their target customers a reference point, making it easier to understand the benefits of Segment.

Step 5 Articulate your value

What: Articulate the value your product provides relative to the alternatives in a way most likely to resonate with each segment.

Why: This is where you bring your positioning home. Having identified the jobs to be done, benefits, customer segments and competitive alternatives, it’s much easier to articulate the value of your offering.

Communicating the value of your offering to a target customer to get them to buy it at a target price.

Example

Let’s look at Segment again. They have identified three customer segments for their platform – Engineering, Product and Marketing and have dedicated web pages articulating the value most relevant to each one.

Customer segment

Value

Engineering

Data standardization Ease of integration Ease of compliance

Single view of your customers Integrate with the best analytics, testing and data tools Cross-team collaboration on analytics

Once you’ve articulated the value of your offering, it’s critical to write it down for the rest of your company. It’s also important to treat it as a living document — your positioning is guaranteed to change over the lifetime of your company. A living document forces you to track changes systematically and provides a record of key positioning decisions. In Part 3, I’ll discuss some of my favorite formats for documenting positioning.

Early stage B2B or developer focused companies that have found their first few customers and believe they’re on a promising trajectory towards product/market fit. Spending time on product marketing without having any early traction is akin to spending time on 5 year revenue projections when you have just a handful of customers. You’ll end up with an elaborate work of fiction that you’ll need to throw away in six months when your understanding of the market inevitably changes.

Ideally, you want to start spending time on product marketing when you believe you’ve found enough customers with similar requirements and characteristics that want to use your product — a customer segment. But more often than not, I’ve seen startups wait too long to start working on product marketing as opposed to starting prematurely.

Why should you hear what I have to say?

I’ve spent the last 3 and a half years in product marketing at Twilio during a time of rapid change and transformation for the company.

We went from having barely any sales force at the time of going public, to growing the sales organization more than 10x by mid-2020. The scope of product marketing broadened from just developer awareness and adoption to prioritizing sales enablement and marketing campaigns focused on business and executive personas.

Some products I’ve positioned and launched:

Programmable Voice: I launched the original public beta of Voice Insights and improved the on-boarding and developer experience for new sign-ups for the Programmable Voice product.

Autopilot: I took the product from beta to GA by formalizing positioning and sales enablement. I was also the PM for the developer experience where I improved the documentation, launched new dev tools and improved the on-boarding experience.

I left Twilio in October 2020 to join Modern Treasury to lead product marketing. I love advising early stage companies on product marketing and go-to-market and invest when it makes sense. There’s more about my startup advising and investing here.

What is Product Marketing?

Communicating the value of your offering to a target customer to get them to buy it at a target price.

Great Product Marketing drives preference for your product in the marketplace. It ensures your target customers think of your product first when faced with the problem it solves.

For example, consider the following problems a software buyer might face and the products that are most likely to come to their mind:

Product

Problem

Stripe

I need to receive payments online

Square

I need to accept credit cards in my store

Twilio

I need to send text messages to my customers

Plaid

I need to link my customers’ bank accounts

DataDog

I need to monitor my cloud infrastructure

Products that are top of mind have great product marketing (in addition to being great products of course).

Product Marketing is the foundation of other marketing and sales activities like demand generation, outbound sales and community evangelism. It determines the core message, channel, target persona and call to action for each campaign. Running a deliberate marketing campaign before your first product marketing exercise is a recipe for failure.

The tactical focus of Product Marketing in a B2B startup changes based on stage — early product/market fit, late product/market fit and growth, and type — primarily top-enterprise sales and primarily bottom-up user or developer focused sales.

Early product/market fit → segmentation, competitive analysis, quantifying customer value, pricing experiments

Late product/market fit → case studies, packaging, campaign planning and prioritization, sales enablement

Primarily top-down sales → case studies, customer advisory boards, webinars, RoI calculators

By ‘early product/market fit’ I’m referring to the stage right after a startup finds their first target customer segment — when it makes sense to start working on product marketing.

Who owns Product Marketing at the early stage?

At the early stage, product marketing needs to be an input to your product strategy. Kicking off a few product marketing activities once you’ve found early traction ensures your product has a strong narrative from day one. It’s also very effective at placing you in your customer’s shoes, forcing you to look at your product from the outside-in.

In the absence of a dedicated product marketer, the same person that owns product management should own product marketing. A generalist marketer can also do a good job provided they’re entrepreneurial and technical enough to have sales conversations with your customers and comprehensively analyze the competition.

If you’ve already raised money, chances are you’ve likely done some foundational product marketing work already. At this stage, there’s likely no difference between your product and your company. Some of the components of the story you’re telling investors can be repurposed in the story you’re telling customers — also known as positioning.

Breaking down Product Marketing

Product marketing consists of four components:

Segmentation, also known as dividing and prioritizing your target market.

Positioning, which determines how everyone at your company talks about the product to customers, whether on your marketing channels, sales conversations or support.

Packaging, which describes different configurations of your features or products customers can buy.

Pricing, which determines what and how you charge for individual products or packages.

You can see each component represented in the definition of product marketing I presented earlier:

Communicating the value of your offering to a target customer to get them to buy it at a target price.

Value = Positioning

Offering = Packaging

Target Customer = Segmentation

Target Price = Pricing

Packaging and pricing are only useful once you have completed segmentation and positioning. Segmentation and positioning are deeply intertwined. They can’t be performed discreetly. You can’t position a product without an audience in mind. And to identify an audience, you need a product and therefore a starting ‘position’. The good news is that your first set of customers are a great starting point for your first segmentation exercise. Positioning and segmentation set the foundation of great product marketing, and I’d argue even great product development.

It’s critical to not get too attached to your segmentation and positioning. Treat them as hypotheses that need to evolve with your business and the market environment.

Positioning and segmentation go hand-in-hand

Positioning can’t take place in a vacuum. Before you can come up with a compelling position for your product, you need to identify a target customer and the problems that matter to them. Looking at the same examples discussed earlier, each company is trying to reach a different target customer with their core product:

Product

Problem

Customer segment(s)

Stripe

I need to receive payments online

Developers, PMs

Square

I need to accept credit cards in my store

Small business owners

Twilio

I need to send text messages to my customers

Developers, PMs

Plaid

I need to link my customers’ bank accounts

Developers, PMs

DataDog

I need to monitor my cloud infrastructure

Developers, IT

Target customers must have one or more easily identifiable features — functions (as shown above), company size, industry, location and even company age — digital native or conventional enterprise, midmarket or SME.

You combine these features to create a customer segment. An example customer segment for Twilio could therefore be developers and PMs at automotive CRM companies.

Segmentation is critical because different customers value different capabilities of your product. They use different vocabularies to think about and describe their problems. You need to position your product differently to each segment.

Conversely, positioning success with one segment does not always translate to another segment. Consider software buyers with the following requirements:

I need software to run my 10,000 seat contact center.

Twilio wants to be the first name prospective customers think of here, but is still a newcomer to the contact center space. A lot of prospects that know of Twilio still only see it as an SMS company. The goal for Twilio with Flex is to position themselves as a serious option in a decades old contact center market dominated by incumbents.

I need serverless infrastructure to deploy my application

When Cloudflare launched a serverless computing platform called Workers, they were entering a crowded space consisting of major cloud platforms on one end and startups like Vercel, Netlify and Serverless on the other end. Workers was also a developer product, a very different persona than the IT or network admins Cloudflare typically sells to.

Their positioning for Workers is quite different from other Cloudflare products:

It has a separate subdomain

Code is front and center

Focuses on specific technical benefits

CTAs point to ‘Start Building’ or ‘Read docs’

Breaking down your TAM into customer segments also helps prioritize product decisions. Sometimes segmentation can even lead you to ignore a number of customer segments.

To summarize and conclude part 1, the goal of product marketing is to drive preference for your product in the marketplace. It is the foundation of your marketing strategy because it helps you systematically identify the most compelling value proposition for a target customer segment. It’s key activities are positioning, packaging, segmentation and pricing. Positioning and segmentation come first, followed by pricing and then packaging.

In part 2, I’ll break down a positioning framework I like using.

Firstly, I wrote this piece almost two years ago but didn’t publish it because I thought it wasn’t very good. But then I read it again yesterday and thought it to be quite well-written! My past self was highly criticaland insecure about my writing. I guess my present self has learned a lot about writing like no one is reading.

Secondly, a lot has changed about the enterprise collaboration market since I wrote this. Slack went public and is trying to become an enterprise social network (?) and Teams seems to be crushing it by using the Microsoft sales machine to prevent Slack from getting into the enterprise and investing in their own dev platform.

And to top it all off, Zoom is entering the chat. Like literally.They’re apparently building more robust chat features that will inevitably compete with Slack.

So if you’re looking for a current take, stop reading! I don’t want to waste your time. But if you’re interested in a snapshot of my thinking circa October 2018, go right on ahead. To be fair, I still think classifying Slack apps into Essential, Internal and Ecosystem apps still makes a lot of sense, and the number of companies primarily building for Slack has only grown since I wrote this post.

To build a sustainable moat, Slack is trying to become the connective tissue of the modern workplace. The Slack API is the lynchpin of this strategy.

Slack’s explosive growth over the past 4 years stole market share from HipChat, resulting in Atlasssian shutting down the product and selling it’s IP to Slack in exchange for a stake in the company. Slack is now dominant with a 70% share of the team chat market.

But what got Slack to its leadership position won’t help it stay there. User experience is not sufficient to build a sustainable moat and certainly not one that justifies a $7 billion dollar valuation. The competition is coming at Slack from all sides. On one side, it is threatened by startups like Flock and Chatwork and more established SaaS companies like Zoho looking to expand into team chat with Cliq. They’re competing with Slack primarily on price.

On the enterprise end, it’s competing with Microsoft Teams and Facebook Workplace. Microsoft is pushing Teams by using existing relationships and contracts and by bundling it into Office 365. They’re also likely to come after Slack’s bread and butter – mid market companies, with their deep pockets, larger sales teams and distribution partners.

To their credit, Slack realized this pretty early on, launching the App Directory in 2015, only two years after the company was founded. From the Verge article that reported on this announcement in 2015:

Slack built all of its initial integrations itself, starting with Google Docs, Github, and a bug tracker, among others. The team’s insight then, which helps explain its meteoric rise, is that those integrations fueled all-day usage of Slack. “The more information you pushed into the messaging system, the more people paid attention to it,” says Stewart Butterfield, Slack’s founder and CEO. “It was a virtuous circle. We didn’t realize how strategic it would be as a business deal until after Slack had launched. And then suddenly it was just very obvious — the more apps we get people to install, the more likely they are to keep using Slack.

In the last 3 years, the Slack API has been used by 200,000+ devs to build 1500+ apps in the directory. While increasing usage and retention may have been the goal of enabling third-party integrations in 2015, I think this thesis has changed considerably since then. The Slack API may have started as a growth hack. Today it is a critical component of the company’s product strategy.

Slack has an intensely loyal user base — most employees would revolt if IT tried to take away their Slack. But sustainable and defensible businesses can not be built on product loyalty alone. They are built by products that excel at locking in customers. These products do more and more jobs for their customers over time, gradually absorbing their customers’ workflows and processes. The more bespoke their implementation becomes, the harder it is for them to churn. Conversely, requiring a bespoke implementation for customers to start seeing any value can be a barrier to adoption. The most successful products are therefore easy to adopt, show value immediately after adoption, and can grow into the organization. They get adopted by more people, customized, inserted into more workflows and ultimately become a critical component of their customers’ operations. Salesforce is a prime example of this. It will never win any awards for design, and with the extremely confusing new Lightning experience, probably not for user experience either. But with the Salesforce APIs, the App Exchange and with products for almost every department and vertical, Salesforce excels at increasing lock-in.

Judging the strength of Slack’s lock-in involves taking a look at the types of apps that are being built with the Slack API. I think they can be divided into three broad categories — Essential Apps, Ecosystem Apps and Internal Apps.

Essential Apps

These are integrations with other staples of the workplace like Google Drive, Zendesk, Salesforce, Github and others. A lot of these are built and maintained by Slack itself, driven by that original insight that pulling in information from other systems people use frequently increases their Slack usage. People often spend more time in these apps than they do in Slack. Making Slack the way users collaborate when using these applications ensures that they still use it even when they’re not actively using Slack. Using the Google Drive integration to create and share docs with colleagues and responding to comments ensures that collaboration on documents happens inside Slack. Adding the JIRA or Trello integration to a Slack channel means project management workflows are driven by Slack, which is used to create, discuss and track new tasks. Slack is becoming the collaboration layer for these applications, even though a few of them have native collaboration features, like Salesforce with Chatter. These apps are essential to make Slack the place where work happens.

Ecosystem Apps

The majority of the 1500+ apps in the App Directory belong to this category. These are integrations with products that use Slack’s reach to acquire users and it’s popularity in the workplace to drive usage. Some of these apps are also being built exclusively for Slack. Take Donut for example, a Slack app that helps employees with on-boarding and building stronger personal connections with each other. It’s particularly useful for remote workforces, using Slack to pair up two random employees each week, making up for the lack of serendipitous interactions that take place when everyone is in the same building.

Developers are an extremely creative bunch. By allowing anyone to build an app, Slack is increasing the chances they use Slack APIs as the outlet for their creativity. I can see a future where an app comes along for Slack that is so unique and valuable in the experience it provides, that people install Slack just to be able to use that app. Platforms benefit when they make it possible for third parties to build highly differentiated apps.

It also allows Slack to observe trends in ecosystem app development in great detail. This provides valuable signals regarding what their users want. If Slack sees a certain type of app gaining adoption with users, they can decide to build it as a feature or even acquire a company if its strategically important enough. Hit applications tend to come from out of the blue. Having an ecosystem is essential to participate in this creative process.

Internal Apps

There are likely orders of magnitude more apps running internally within different teams than the 1500+ apps in the App Directory. They can be as simple as a Zapier integration or as complex as a custom built incident management workflow. I think these types of apps tend to have the most lock-in value. They tend to be highly customized and are proof that Slack has become so integral to the operations of a team that they are willing to invest developer resources to build custom software around it. Once in place, these integrations are extremely difficult to displace. Employees get trained to use them and grow accustomed to them. Companies also want to minimize the developer resources they invest on non-revenue generating software. Prioritizing building a replacement, either outside of Slack or on a competitor is always hard to justify. Having custom integrations in each department effectively compounds this lock-in — there’s more people to convince and more code to replace. While Slack hasn’t made any data on the state of internal integrations publicly available, its clear from their latest positioning that they’re emphasizing the value of building internal integrations.

Conclusion

The Slack API allows anybody to build an app for Slack. It has great documentation, tutorials and best practices. Initiatives such as this public roadmap for the Slack platform and a new developer conference are indications that the company is serious about developer relations.

I think Slack has the opportunity to shape the very nature of work. It’s already well on its way to becoming the collaboration center of the modern workplace. The next step is to create an entirely new category of products and experiences for the workplace, one that can only be built and delivered over Slack. I don’t know what this ultimately looks like, but I can see early signs of this. More and more products like Donut and Niles, which adds chats to a team wiki, making it easier to document tribal knowledge, are being built that are (for now) unique to Slack. Locking-in users is ultimately critical because business applications are playing a zero-sum game. Users have a finite number of jobs-to-be-done, and a finite amount of time to do them. Every minute a user spends in Slack is a minute not spent using another product.

Developers are an even more scarce resource than users. Investing in documentation, education and developer relations is the right start, but won’t be sufficient in the long run. Slack needs to provide them with business models to successfully monetize their applications. This is the final piece of the puzzle in my opinion. Allowing developers to build sustainable businesses on top of Slack is critical to making it a true platform.

Throughout my time at Twilio, I’ve often wondered why some software infrastructure companies become massive businesses while others falter. What is it about the nature of certain products and the markets they target that makes it possible to build large infrastructure platforms? This post is an attempt to structure what I’ve learned about this question and was prompted by a series of conversations I’ve had recently with early stage API infrastructure companies about product and go-to-market strategy.

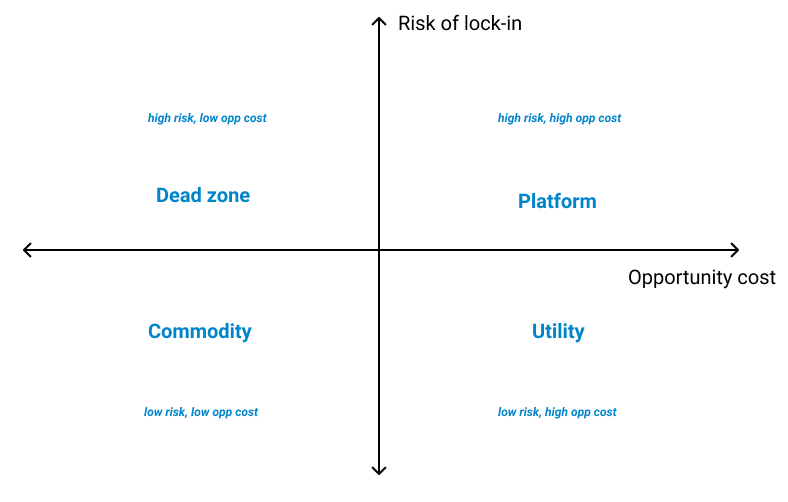

In my opinion, your startup’s target market must have the following characteristics for it to turn into a massive business:

The risk to the customer’s business of being locked into your infrastructure must not be prohibitive.

The opportunity cost of building the same infrastructure in-house must be high enough to consider buying it from a third-party.

There need to be enough customers that meet criteria (1) & (2) willing to pay what’s needed to support a market for it.

Characterizing API infrastructure opportunities by opportunity cost and risk of lock-in

Startups that build APIs for problems that have a high opportunity cost to solving in-house relative to the risk of depending on a vendor have the highest chances of breaking out to become massive companies. Low opportunity costs mean your customers can easily build the same infrastructure in-house, and a low risk of lock-in means they can always switch you out. The sweet spot lies in providing infrastructure that’s hard to migrate from, resulting in a high risk of lock-in, but provides substantially more value than the opportunity cost of building in-house.

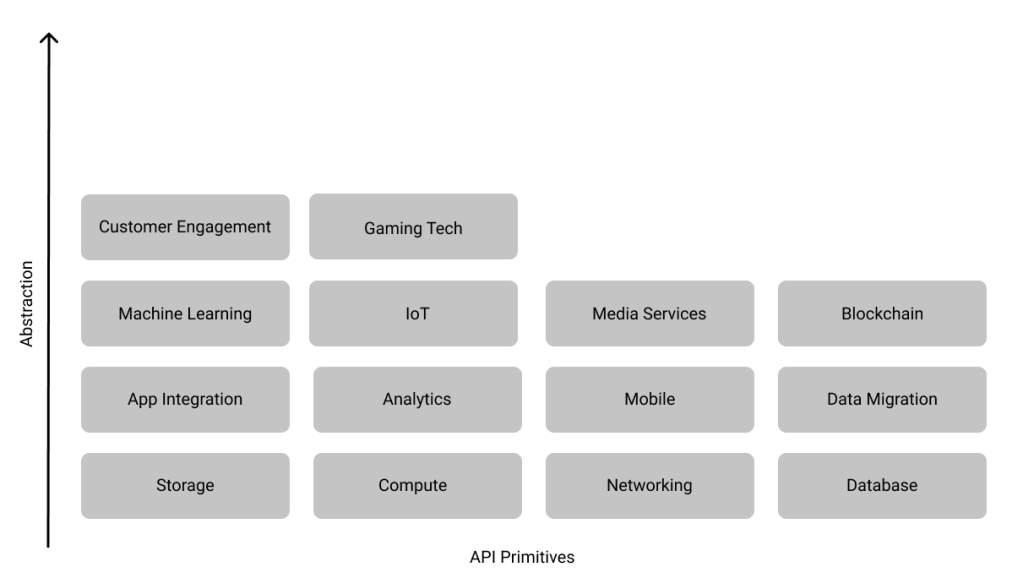

To begin exploring this question in detail though, you need to start with the company that started it all — Amazon Web Services.

1. Land and expand

The advantages of building on a cloud platform are clear as day today. For startups and increasingly for enterprises that need to move to digital business models, using APIs instead of setting up servers turns upfront capital costs into ongoing operational costs, provides instant scaling and eliminates the overhead of maintaining data centers. Even the most sophisticated companies will think twice before building their own data centers today.

If you trace the trajectory of products launched by AWS since they announced SQS in 2004, a pattern emerges. Over the years, AWS has moved up the application stack with new releases to provide infrastructure that is tailored to solving increasingly specific software development problems. These APIs are more opinionated i.e. they force you to build software in a certain way, and tightly integrated with AWS infrastructure, but also a lot easier to use. Jerry Hargove has drawn up this fantastic timeline of every single AWS launch since 2004 and grouped them into categories.

Today, developers can build applications on AWS with APIs providing different levels of abstraction. If you’re looking to build a video streaming application, you can directly use AWS Media Services without worrying about the underlying transcoding, storage and bandwidth infrastructure. But, if you’re looking for more control over your application, perhaps you need to run a custom transcoder optimized for your use case, you can build a video streaming stack using EC2, S3 and CloudFront. I arranged the categories Jerry uses by the general level of abstraction provided by it’s members to illustrate my point. I didn’t consider newer bets like AWS Ground Station or AWS RoboMaker, or horizontal utilities like Developer Tools or Cost Management.

AWS APIs by level of abstraction

AWS APIs that provide more abstraction generally charge higher prices because they can significantly simplify application development and decrease release times. They probably also have higher gross margins for AWS.

This general pattern — starting with lower level APIs, raw compute, storage and networking in AWS’s case, and moving up the stack over time isn’t unique to AWS. Almost every single successful API company founded since the advent of public cloud platforms has followed this strategy.

Twilio’s first product was an API for making and receiving phone calls. Their second product was an SMS API. Since then, they’ve expanded to provide dedicated APIs for two-factor authentication, video conferencing, VoIP, WhatsApp and in-app chat. Recently, they moved even further up the stack with Flex, a programmable contact center that bundles these APIs together under a customizable UI framework.

Stripe’s first product was an API for accepting payments. When they started seeing a lot of traction in e-commerce, they launched a UI framework to make building checkout experiences easier. When they saw a lot of traction from marketplace companies, they built Connect to simplify on-boarding and verifying sellers and routing payments. Since then, they’ve launched APIs for subscription and invoicing, fraud detection and card issuance.

Segment started off providing a unified API for ingesting customer and usage data from multiple sources and loading it into different business analytics tools. Today, they’ve built products that aggregate this data to provide a 360-degree view of each customer, allowing businesses to enrich existing customer data, build audiences in real time and create personalized experiences.

DataDog’s first products were monitoring APIs for virtual machines and cloud instances. Since then, they’ve expanded to other cloud backend configurations like containers and serverless, while also moving up the stack to provide logging and monitoring solutions for middleware and applications.

This ability to land and expand is what separates the wildly successful infrastructure companies from those that fail to take off. This expansion happens horizontally, as more teams come to rely on their API and as they provide APIs at similar levels of abstraction for adjacent use cases, and vertically, as their customers start adopting higher level APIs to solve more specific problems. The beauty of this model, if you can get it right, is that all you need to do to identify new product opportunities is closely observe what applications your customers are building. A large enough number of customers building the same types of applications usually represents an opportunity to provide a higher-level API. This expansion also makes their infrastructure harder to replace, resulting in stellar revenue growth rates and net dollar retention numbers.

I think there’s a more fundamental question you need to ask then to answer the original question — why do some API infrastructure companies land and expand successfully? It starts with understanding the alternatives available to their prospective customers.

Every SaaS product’s toughest competitor is the customer not buying! The hardest customers to sell to think they don’t even have the problem your product solves. What’s every infrastructure product’s most formidable competitor then? Alongside not buying, it’s the customer deciding they can build the same capabilities in-house instead of integrating with a third party.

A customer buys infrastructure if the risk of being locked-in to a vendor is lower than the opportunity cost of building it in-house. API infrastructure companies that demonstrate enough value to overcome the perceived risk of lock-in find it easier to land within their customer’s application stack, expand and become massive companies.

2. Vendor lock-in dynamics

The more reliant a company becomes on a third party, the harder they find it to replace them. This risk isn’t unique to software infrastructure. But a thorough understanding of the risk of vendor lock-in from the customer’s perspective is the most important input to the strategy of any API infrastructure company. This risk is higher if the third party isn’t completely modular i.e. swapping them out is expensive, time-consuming and can have second or third order effects that are hard to predict.

Apple’s decision to move away from Intel is a classic example of vendor lock-in gone wrong. They’re replacing Intel’s chips with their own A-series chips (the same chips that power iOS devices) in all new Macs released in 2021 and beyond. This is going to be a complex transition for Apple because the A-series chips are based on ARM while Intel’s chips are based on the x86 architecture. Apple is bringing chip design in-house because Intel has fallen far behind TSMC in processor node size. TSMC started working on 5 nm chip this year while Intel is still stuck producing 14 nm chips. Intel was also increasingly the bottleneck for Mac innovation — Retina displays took longer to arrive on the Mac than on the iPhone because Intel’s production of 14 nm chips was delayed. Replacing Intel gives Apple full control over the entire Mac stack, allowing them to optimize performance and build features on their own timeline. The risk of depending on Intel ultimately wasn’t worth the benefits.

I’ve most frequently seen four types of vendor lock-in with software infrastructure companies.

Tightly coupled architectures

Economies of scale

Developer experience

Network effects

The lock-in can be quite formidable if more than one type is in play.

Tightly coupled architectures

If using a vendor requires you to explicitly design your software within the constraints of their API, your architecture can get tightly coupled to theirs. The degree to which this happens is hard to assess when you first make that decision because the immediate benefits — speed and implementation costs, are usually obvious, and vendors put a lot of work into making their APIs extremely easy to adopt. It’s only as you scale does the extent to which you’re coupled starts becoming obvious.

Implementing on AWS is the most obvious example here of making a decision that leads to tight coupling. It can be extremely hard to move off AWS, especially if you’ve come to rely on their higher-level APIs! Google’s decision to open-source Kubernetes was specifically targeted at this dynamic. Containers make it significantly easier to run software on multiple cloud providers.

Economies of scale

This dynamic comes into play typically when the service provided by the API infrastructure company has a hard cost to deliver. Take Twilio, Stripe and Cloudflare for example. Each company has an underlying cost to deliver their services, in addition to the cost of their own software and overhead. With Twilio, it’s the cost of text messages and voice minutes, Stripe it’s payment processing fees to Visa and MasterCard and with Cloudflare it’s bandwidth. As these platforms scale, they’re able to negotiate better terms with their suppliers, which they can then pass on to their customers. For a customer, going directly to their suppliers will result in higher prices because most companies can’t match the scale of these platforms.

Developer experience

Developers are increasingly decision makers, or at least important influencers in most software purchase decisions today. This is especially the case with software infrastructure companies. Building APIs that developers love and rely on can also be a significant source of lock-in. And it’s not just about great documentation, building a great community or ease of use. It’s also about how embedded your product can get in the development workflow. This is why so many API infrastructure companies have command line interfaces and support for tools used for continuous integration and continuous delivery pipelines.

Network effects

Network effects are less common because most API infrastructure companies operate multi-tenant systems designed to separate customer data as much as possible. They also don’t typically facilitate transactions between customers on the platform. But network effects can manifest on the supplier side and become a significant source of lock-in. Plaid is a great example of this. For each new financial institution they add to their platform, the value of choosing Plaid over a competitor increases.

3. Risks from vendor lock-in

If these lock-in dynamics create opportunities for infrastructure companies, they create risks for their customers.

Execution risk

Scaling risk

Cost structure risk

The greater the perceived risks, the higher the value delivered by your infrastructure needs to be.

Execution risk

What happened with Apple and Intel is in a sense a great example of execution risk. As Intel struggled to keep up with TSMC, Apple realized they stood to gain more by bringing chip design in-house and outsourcing manufacturing to TSMC than relying on Intel for both design and manufacturing. Not only do they now get Intel’s margin on the chips, they don’t have to be constrained by Intel when launching new features, ensuring incidents like the delay on shipping Retina screens in 2015 would never take place.

When a company buys infrastructure instead of building it in-house, it’s making a bet on the vendor’s vision and ability to execute on their roadmap. The last thing they want is to depend on a vendor that can’t keep up with their roadmap. This is less of an issue for established infrastructure companies, but for startups allaying these concerns upfront is critical.

Scaling risk

The same calculus applies to the vendor’s ability to scale. Companies buying infrastructure want to know whether it can handle their existing transaction volume, manage volatility in volumes and add capacity to support increases in volume over time. Established infrastructure companies like Twilio, Stripe and DataDog got around this problem in part by first selling to startups. As WhatsApp, Uber, Lyft and AirBnB started growing rapidly, they scaled in tandem to build the capacity required to support larger enterprises later on.

Not all API infrastructure companies need to sell to startups or individual developers at the beginning. In fact, most companies are unlikely to have an addressable market with a long tail of small customers. If you’re selling to enterprises from day one, structuring the engagement like a professional services or custom software development contract can be effective at addressing this concern, while also giving you a deeper understanding of their requirements.

Cost structure risk

When a company decides to use Stripe instead of becoming a payment facilitator themselves, they’re giving up the ability to negotiate favorable payment processing fees with the card networks. This is a major selling point for long tail developers and small and medium businesses. It’s also a compelling reason to use Stripe for larger businesses that don’t have the appetite to integrate directly with banks and card networks. But for businesses processing hundreds of millions of dollars every year, each cent they pay Stripe on top of the fees charged by Visa and MasterCard starts to add up. Bringing payment processing in-house starts to look very attractive. Startups like Finix have emerged to allow companies to do just that without building a payments processing stack from scratch.

4. Opportunity costs

The opportunity cost of building infrastructure in-house is essentially the cost of the engineering team needed to build, operate and maintain it not working on something else. The calculus is straightforward — is it a better investment to have expensive engineers build software you could just plug in from a third-party instead of working on features that will differentiate your core product? There’s also an element of execution risk here — once built, can your team add features and scale faster than a third-party whose entire business depends on providing the best infrastructure possible?

The opportunity cost is inversely proportional to how strategically important the infrastructure is to the business model of the company. Taking an extreme example, Netflix would never use a third party video streaming API even though it could significantly lower their engineering costs. The opportunity cost is non-existent here because of how critical owning the end-to-end video streaming infrastructure is to their business. WhatsApp is an example on the other extreme — SMS verification is a core part of their user on-boarding flow. But the opportunity cost of directly connecting to every single carrier in the world is too high! It makes more sense to use Twilio than divert engineering resources from working on the core product. That’s also why WhatsApp, or any other chat app for that matter will never use a third party for their real-time messaging infrastructure.

In my experience, it’s hard for customers to measure opportunity costs systematically and objectively. They can only be considered when the build or buy decision is being made and depend on business priorities, budget constraints, market conditions and with larger companies, internal politics.

5. Clearing the threshold

It follows then that customers only derive value from API infrastructure if the opportunity costs are higher than some minimum threshold and the risk of lock-in is lower than some maximum threshold. Understanding these thresholds for your addressable market is critical to determining if you have product-market fit.

Here are a few questions I’ve found useful when evaluating the target market for an API infrastructure company.

Vendor lock-in

What scale are your target customers operating at? Typically expressed in usage or API calls.

Can your platform handle their scale over time?

How complex is the integration? Focus on how much additional work the customer needs to do to start seeing value from your API. Do they need to build a UI or integrate with Salesforce for example?

How sensitive is the data they’re sending you? Are you storing it?

How much is your roadmap and vision aligned with theirs?

What portion of their service delivery cost is your infrastructure?

Opportunity costs

How strategically important is this functionality?

How large an engineering team do they need to build and operate this in-house?

Is this something their engineers are excited to work on?

Are there on-going non-engineering costs like regulatory compliance, security overhead and complex contractual relationships?

Does building require maintaining a large number of third-party integrations?

Will cost and performance improve meaningfully with constant optimization

Thanks for reading — this post may have gotten a bit wonkier than I intended! Please send your thoughts and feedback to me on Twitter: @pranaveight.

Peloton went public in September 2019. Since then, barring a blip in March when the entire market sold off, the stock is up 70%. It’s winning big in the quarantine economy as people looking for alternatives to gyms, sports and fitness classes have turned to its slick connected bikes and treadmills and streaming content. You can directly stream live and recorded fitness classes produced by Peloton on screens attached to the bike and treadmill, or you can purchase a standalone digital subscription that gives you access to the same content. Their streaming service is available on all major platforms. The content is always fresh and engaging, with many Peloton instructors becoming social media celebrities over the years.

Quarter

July – Sept 2019

Oct – Dec 2019

Jan – March 2020

Revenue (millions)

$228.00

$466.30

$524.60

Connected Fitness Product Revenue (millions)

$157.60

$381.10

$420.20

Digital Subscription Revenue (millions)

$67.20

$77.10

$98.20

Peloton Quarterly Revenues

Most startups are supposed to fail, and this was especially true for Peloton. When CEO and co-founder John Foley was looking for investors after burning through a seed round trying to prove out the concept, he was rejected by both fitness industry insiders and venture capitalists. He even tried to partner with Flywheel, one of the pioneers of the studio cycling craze. From this Inc.com from 2016 –

Meanwhile, Foley approached Flywheel about joining forces. The idea was that Peloton would continue building out its business model, but become part of Flywheel and use its classes as content. The deal fell through. (Zukerman (Flywheel founder) says neither she nor current management was involved in any talks with Peloton. Foley says he dealt with the company’s prior chairman, David Seldin, and former CEO, Jay Galluzzo.)

He decided to go it alone after Flywheel turned him down. Similar discussions with SoulCycle also didn’t go anywhere (they must be kicking themselves right now). Peloton would build the bike hardware and software and create the streaming content from scratch. This new direction for the business made the already challenging task of raising funding for a business without any precedent even harder.

From the same Inc.com profile:

It was true that Foley could offer no research to convince potential investors that a market existed. He was relying on his gut instinct, which told him that there had to be lots of people like him out there who would love to own what he was building. Ironically, more than a few VCs told him, “I’m not going to invest, but when you build this, let me know, because I want to buy one,” he says.”

After a $3.5 million Series A and a relatively underwhelming kickstarter campaign in 2013, Foley realized Peloton needed to get into retail for the concept to take off. His intuition was that early adopters needed to physically experience the bike and streaming classes to be convinced to pull the trigger. They also realized they couldn’t outsource delivering the bike to third-party logistics companies. Assembling and setting up the bike was a critical part of the experience they had to bring in-house to ensure quality.

In its first two years, Peloton had gone from a company trying to build a connected bike and video streaming infrastructure to a retail company with its own logistics arm. But they weren’t done! They still needed cycling classes to stream and SoulCycle and Flywheel refused to partner with them. So Peloton built their own content production operation and started directly hiring instructors.

Today, Peloton is a fully integrated provider of at-home fitness experiences. They manufacture the bikes themselves (having purchased Taiwanese bike manufacturer Tonic in October 2019), deliver the bikes using an in-house logistics team, operate retail stores and live studio sessions in NYC and London, produce high quality fitness videos and operate streaming infrastructure that delivers this content to their bikes and treadmills but also phones, tablets, computers and TVs all over the world.

This has allowed them to build a business with incredible growth and unit economics. Peloton today has two types of customers — ‘Connected Fitness Subscribers’ that purchase the bike or treadmill and a streaming subscription, and ‘Digital Subscribers’ that only purchase the streaming subscription. The former pay $39/month for access to classes and profiles tracking metrics and performance for the entire family, while the latter pay $13/month for individual subscriptions to streaming content only.

[CAC] Hardware gross margins are funding capital-efficient customer acquisition

Quarter

July – Sept 2019

Oct – Dec 2019

Jan – March 2020

Connected Fitness Subscribers

562,774

712,005

886,100

Connected Fitness Subscribers YoY Growth

26.52%

24.45%

Digital Subscribers

105,856

109,000

176,600

Digital Subscribers YoY Growth

2.97%

62.02%

Total Subscribers

668,630

821,005

1,062,700

Total Subscribers YoY Growth

22.79%

29.44%

Connected Fitness Product Gross Margin

43.00%

40.50%

45.30%

Connected Fitness CAC (Weighted Average)

$1,293.18

$1,031.59

$461.34

Digital FItness CAC (Weighted Average)

$101.75

$21.73

$179.14

CAC

$1,394.93

$1,053.32

$640.48

GM per incremental connected fitness subscriber

$1,314.05

$1,034.27

$1,093.37

Approximate CAC and GM

Peloton is a high CAC business. The bikes and treadmills are expensive and target affluent customers that cost a lot to reach and serve. The digital subscription is more affordable, but the content is designed to appeal more to urban millennials that tend to have more fitness alternatives. It’s also a novel concept, requiring generous promotional offers and perks like 0 APR financing and free delivery and installation services that all roll up into CAC. But high CAC by itself isn’t a problem. It needs to be looked at in the context of the company’s other unit economics.

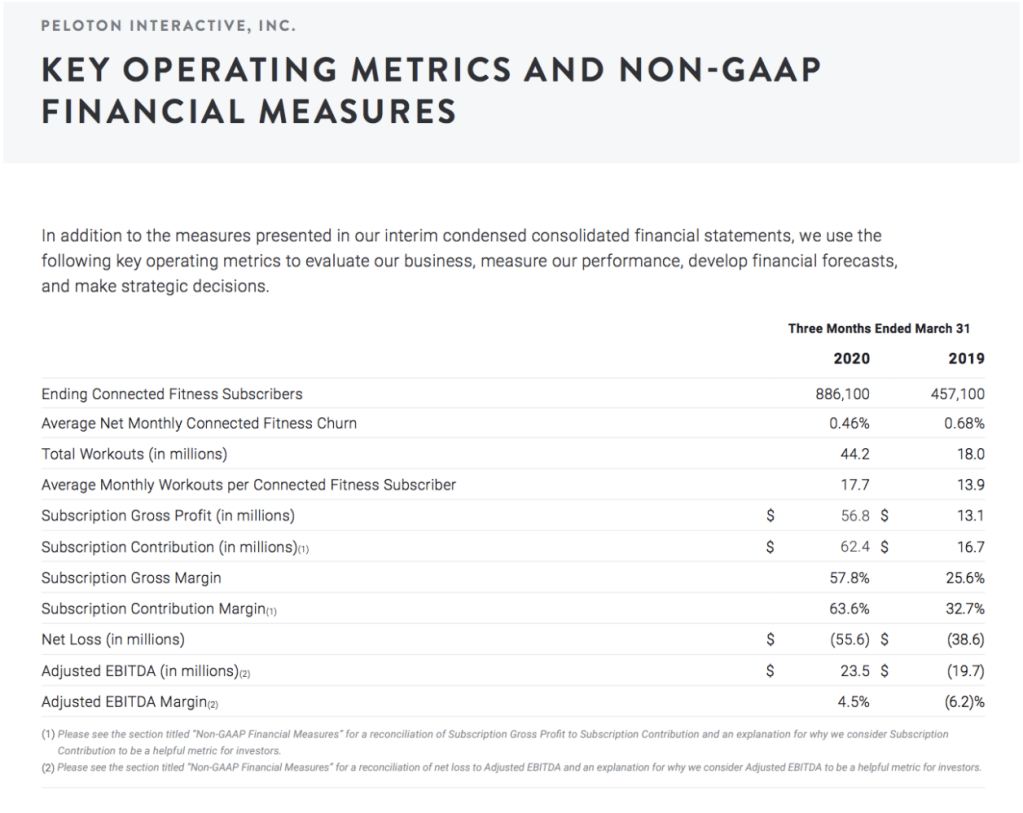

As Ben Thompson pointed out in his analysis of Peloton’s S-1 (paywall), the gross profit they made on each bike sale more or less made up for the cost of acquiring that customer which means all subscription services revenues, less the cost of producing and delivering that content, went straight to the bottom line!

This has continued to be the case in 3 out of the 4 quarters since the company went public. They don’t directly report a CAC in their 10Q, so I had to estimate it by dividing each quarter’s sales and marketing expense by the new subscribers added in that quarter. They also started disclosing how many subscribers they added for each category only after going public. Since these customers are purchasing fundamentally different products (to start at least), I decided to assign a separate CAC for each category weighted by their total net additions in the quarter. Unfortunately because they didn’t disclose digital subscriber numbers prior to Q1 of the 2019 calendar year year, I could only start comparing weighted average CACs from Q3 2019 onwards.

Looking at the combined CAC for both types of customers, this trend has continued, and seems to be improving. Peloton added ~149k Connected Fitness Subscribers in Q4 2019, bringing in $154m in gross margin dollars and spent $160m on Sales and Marketing. They added ~174k in Q1 2020, bringing in $190m in gross margin dollars and spent $154m on Sales and Marketing. Their ability to continue selling bikes and treadmills is critical to their ability to keep acquiring customers in a capital efficient manner. They recently paused treadmill delivery because of ‘the high touch nature of it’s assembly’. Some skeptics speculate it could also be because treadmills haven’t sold very well. I couldn’t find any definitive information on this though.

[Growth] Content and community are the company’s future

For what’s likely the first time in the company’s history, Digital Subscribers grew faster than Connected Fitness Subscribers in Q1. The pandemic obviously played a huge part in this, and it seems unlikely they’ll see a jump this big in quarter-over-quarter growth rates again, but Peloton’s starting to look more and more like the Netflix of fitness. Foley at least seems to think that the subscription business could be more valuable in the long run. From this Forbes piece before their IPO:

“It’s funny. Internally, I happen to be one of the people in the leadership team to think that [digital subscriptions] could over time eclipse the the core connected fitness business,” Foley says. “We are going to be watering the acorn that is a pure digital business and bringing that to as many people as possible.”

Peloton offers all kinds of live and on-demand fitness classes, which are then curated into collections and challenges.

They’ve built a community of 1 million members around this content. Members can ‘wear tags’ to show their affiliation with physical communities, causes and identities. They earn badges for hitting milestones in different work out categories. While a thorough breakdown of Peloton’s community features and dynamics, both within the app and on social media, is a topic for a separate post, it’s clear Peloton has a massive opportunity here. They have a heavily engaged user base, with average monthly workouts per user trending upwards even as the company adds more customers at a record clip.

Finally, the entire experience would suffer significantly in the absence of great instructors and Peloton seems to have the best. Instructors like Robin Arzon and Alex Toussant have large independent social media followings — 436k and 177k followers on Instagram each. They also have exclusive contracts with the company as far as I can tell, and also get some of their compensation in stock, heavily incentivizing them to help the company succeed. They’re always promoting Peloton when they promote themselves. It’s not that different from professional sports — when Russel Westbrook or Ronaldo post something online, it’s free marketing for the Rockets or Juventus, but also for their sports leagues because there’s only one place you can watch them play. Instructors help Peloton acquire new customers organically and their celebrity status keeps existing customers loyal.

Avg Monthly Workouts per Connected Fitness Subscriber

11

12.6

17.7

S&M expenses (millions)

$77.60

$160.50

$154.80

Connected Fitness Payback Period (months)

33.16

26.45

11.83

Digital Subscriber Payback Period (months)

12.43

2.60

21.68

Avg Net Monthly Connected Fitness Churn

0.90%

0.74%

0.46%

Connected Fitness Lifetime (months)

111.11

135.14

217.39

Subscription Contribution Margin, Engagement and Churn

Subscription Contribution Margin is a measure of how much streaming revenues contribute to the bottom line after subtracting the costs of content production.

Peloton’s on a great trajectory here, with an increase of 30% year over year. It’s held steady on a quarter over quarter basis with the company attributing that to expanding to new fitness categories. They expect this to continue being the case for at least the next quarter, guiding to a Subscription Contribution Margin of 63.0% to 64.0% in their most recent shareholder letter. To me, the fact that they expect margins to stay unchanged is a sign that they’re continuing to aggressively invest in fitness content.

Leveraging the fixed costs of content production is key to building a durable moat. When combined with their capital-efficient customer acquisition and low churn, each new Peloton customer gives them additional dollars to invest in customer acquisition and content production. This is a strong positive feedback loop that could allow them to out-execute the competition in the near term.

Peloton’s Moat

Who does Peloton compete with? If you drink the company’s kool aid, they have no real competitors. Peloton is the only fully integrated technology-media-software-product-experience-fitness-design-retail-apparel-logistics company. This image is from their S-1.

But it’s obvious they’re in direct competition with gyms and boutique fitness classes. Anyone skeptical of the company will also note that the at-home fitness industry has been around for decades.

NordicTrack has been around since 1975 and makes treadmills, bikes, ellipticals and strength machines. Their bikes and treadmills are a lot cheaper than Peloton’s – $1999 vs $2245 and $2999 vs $4295 respectively. They also have a streaming service called iFit that comes bundled with the equipment. As far as I can tell, they don’t sell a standalone subscription. Unfortunately NordicTrack is privately held so I couldn’t easily find their operating metrics.

But Nautilus Inc, which makes treadmills, ellipticals, bikes and recumbents, is a public company. Their bikes and treadmills are even cheaper – $699 vs $2245 and $1,399 vs $4295. Notably, Nautilus is just an equipment company — they don’t have a community, instructors or a streaming service. They have slightly lower gross margins than Peloton. From their latest 10-Q:

Gross profit decreased by $0.2 million, or 0.7%, for the first three months of 2020 to $35.6 million, or 38.0% of net sales, compared to gross profit of $35.8 million, or 42.5% of net sales, for the first three months of 2019. The decrease in gross profit dollars was primarily due to lower gross margin percentages in both the Direct and Retail segments. Gross margin percentage points decreased by 4.5% for the first three months of 2020 compared to the first three months of 2019 primarily due to unfavorable sales mix and higher landed product costs.

And then there’s Echelon, a startup based out of Tennessee, that Peloton sued last year for trademark infringement. Their most expensive bike costs $1999.

Given this landscape, I think Peloton’s moat comprises of it’s instructors, community, continuing to leverage content production costs and maintaining hardware gross margins.

Instructors are the most important part of the experience, and by tying them to exclusive contracts Peloton ensures their classes are highly differentiated. Their community can generate strong network effects, and I believe they’ve only scratched the surface here. I won’t be surprised if they go on to challenge a company like Strava, or even acquire them. Continuing to leverage content production and maintaining hardware gross margins is going to be a lot harder. As the at-home fitness market expands post-COVID, it’s quite likely a deep pocketed competitor will enter with a cheaper bike and content that has a similar production value.

For now though, a lot is going in their favor. SoulCycle has been caught completely flat-footed by the pandemic. Delays in delivering their new bike are causing even the most loyal SoulCycle fans to switch:

“I was waiting, waiting, waiting because I wanted the SoulCycle bike to come out. They released the pre-order, and I realized they didn’t service the area that I’m in,” said Erica Baddley, 26, who used to routinely drive 45 minutes from her home to the nearest studio, in Denver. “I would have been first in line.” Four weeks ago, Ms. Baddley ordered a Peloton.”

The same article also estimates that the American fitness club industry lost $3.5 billion in revenue between March 26 and May, which could rise to $6 billion if gyms stay closed through June 1. And even if they do open, there’s no guarantee customers will return.

Looks like Peloton is in the right place at the right time with the best possible product. 2020 is going to be an eventful year for them.

This post is for informational purposes only, you should not construe any such information or other material as investment advice. I may have held positions in Peloton stock at the time of writing.

Truth be told, I started learning about the business in earnest only after getting a masters degree in business and engineering. It started with regularly digesting newsletters, blogs and podcasts from Ben Thompson, Horace Dediu, Tom Tunguz and others. It really started picking up momentum when I learned how to use Tech Twitter productively, and discovered folks like Tren Griffin, Josh Wolfe, Patrick O’Shaughnessy and others. I’m quite pleased that I have managed to situate myself within so many different information flows today (twitter, twitter DMs, newsletters, whatsapp groups), that I have a lot more content to go through than time!

Just take a look at my reading list right now:

(I find Pocket invaluable because I always find interesting stuff faster than I can consume it)

All of this to say that without using the Internet to enroll myself in a lifelong business school education, I would have never learned that you can’t really understand business strategy without understanding unit economics. My fascination with unit economics only started last year leading up to the Lyft and Uber IPOs. There were two extreme, diametrically opposed narratives at play – the techno-optimist one that high growth rates and large markets justify high burn rates and the more conventional one that questioned if these companies could ever turn EBITDA positive. The first one focused on revenues and the second on profits and meanwhile, tech twitter was inundated with superficial articles focused on how much money these companies were making or losing.

I started having a million questions about the notion of a ‘business making money’, something I hadn’t really thought about deeply before. I’d always figured that as long as a startup sold something for more than it bought that thing, and had a large enough market and enough cash to burn as it grew, it would end up successful. It turns out, figuring out whether a startup has a viable business model is a lot more complicated than that, and it starts with unit economics.

It also turns out that while there is a relatively straightforward and well-defined theoretical framework for understanding the unit economics of a business, doing so in practice is a lot harder. Getting the right data, even from public companies, can be problematic. Each company can also report the same underlying metrics differently, making benchmarking an issue.

In this post, I’ve briefly described the theoretical framework I’ve learned over the last year. My plan initially was very academic — I wanted to study the framework’s history and how it’s formulae were devised. But as I dug deeper, I realized that to really understand how unit economics make or break a business, you need to study actual businesses (obviously).

That’s why I plan on studying the unit economics of different types of subscription businesses in subsequent posts.

The Theory

Why do unit economics matter?

A business has bad unit economics if it’s selling a product or service for lower than it’s true cost — the proverbial ‘selling dollars for 90 cents’. As Fred Wilson points out:

“Where I come out on this issue, and always have, is that growth has to be responsible (positive unit economics on growth spend) and that the path to profitability needs to be well in sight. I would add to those two constraints that a management team ought to be able to get a business profitable in a pinch without killing the business, if necessary. Clearly these “rules” should not apply to very early stage companies. They become relevant and possible once a business has a growing customer base and revenue stream.”

What does positive unit economics on growth spend mean? Turns out, there are a number of variables that ultimately decide the true cost of product or service delivery. The best place to learn about unit economics on the Internet is Tren Griffin’s blog 25iq. In fact, to write this piece, I tried reading everything he’s said on the subject. I’ll probably be rereading it from time to time. It’s so information dense that you can read it from a different perspective each time and learn more.

In this post analyzing the economics of Amazon Prime, he points out that the unit economics of a business consists of the following factors:

A customer acquisition cost (CAC)

An average revenue per user (ARPU)

A gross margin

A customer lifetime (which is a function of customer retention/churn)

A discount rate.

A business has viable unit economics if it has a positive customer lifetime value or LTV. In his now famous post on the dangers of mistaking LTV maximization as business strategy, Bill Gurley describes the following equation for calculating LTV:

The gross margin (sometimes also described as contribution margin) is the difference between the revenue contributed by a user in a certain time period and the cost to deliver the product or service to the user, and decides how much cash each user is periodically contributing to the business. The SAC or subscriber acquisition cost is the same as CAC or customer acquisition cost. ‘N’ here is the customer lifetime and WACC is the weighted average cost of capital, also generically referred to as the discount rate.

How can businesses control their unit economics?

The short answer is they can’t, at least not directly. It’s extremely important to separate the process of finding viable unit economics from the formula itself. Building a business around optimizing the formula is bound to blow up in your face because key input variables — revenue per user, customer lifetime and customer acquisition costs are interdependent, not independent. Trying to move one variable usually ends up moving another, and usually not in the direction you’d want. As Gurley points out in the same post:

“Some people wield the LTV model as if they were Yoda with a light saber; “Look at this amazing weapon I know how to use!” Unfortunately, it is not that amazing, it’s not that unique to understand, and it is not a weapon, it’s a tool. Companies need a sustainable competitive advantage that is independent of their variable marketing campaigns. You can’t win a fight with a measuring tape.”

Tren Griffin offers the following advice to startups specifically:

“If you’re an early stage SaaS startup, still trying to get product/market fit, or experimenting with different ways to make your marketing and sales predictably repeatable and scalable, it is useful to play around with CAC and LTV to get a feel for where you are. But it’s important to note that these formulae will only yield meaningful results when your sales and marketing process and costs are predictable and scalable. Instead of spending too much time obsessing over CAC and LTV, rather focus your energies on solving the problems of improving product/market fit, and making your customer acquisition repeatable, scalable and profitable.”

Churn and payback period

The payback period is the time it takes to recover CAC. Shorter payback periods are always better because they make it possible to use operating revenues to fund growth, allowing the business to preserve cash on the balance sheet. They also tend to have a flywheel effect where the more you spend the faster you grow because each incremental customer brings in more revenue that you can spend on growth. There’s one caveat though — it only makes sense to compare payback periods between businesses selling similar products or services. Larger transaction sizes result in larger CACs and longer payback cycles. Just because the payback period of a subscription streaming service is a lot smaller than that of an enterprise software product doesn’t mean it has better unit economics.

However, it’s really important that regardless of the type of business, the payback period is shorter than the LTV. If customers churn before they are able to pay back their acquisition costs, the business is in big trouble. It has what’s known as a ‘leaky bucket’ problem. In this scenario, continuing to invest in customer acquisition is actually detrimental to the company, since each new customer eventually sucks cash out of the business!

Subscription duration, retention and the value of optionality

Convincing customers to subscribe requires providing a product or service that is more valuable to them than the combined value of the next best alternative available and the optionality of not commiting to a monthly fee.

That’s why a lot of businesses offer a free trial, allow customers to cancel any time and rarely require a longer commitment than one month. The greater the perceived commitment, the more the business must spend on customer acquisition to convince the customer to subscribe.

“Why do some businesses sell subscriptions but allow a customer to cancel at any time? Because the longer the customer is asked to commit to the periodic relationship, the more financial incentive the customers must be given to do so or the more in sales and marketing will be required to acquire the gross customer addition. In other words, the longer the commitment and the higher the commitment in terms of dollars, the higher the customer acquisition cost (CAC) will be.”

In Practice

I’m going to test these concepts by examining the unit economics of a few well-known public subscription businesses in the consumer and B2B spaces. Luckily for me, a lot of people have done fantastic work dissecting their business models. What follows in subsquent posts is a mostly my commentary on their analysis. I’ll be starting off by looking at Peloton.

Every December or January, like most Indians living in the US, I make the long trip back to India to visit family and friends. It usually consists of switching off and relaxing at home, vacations with family or catching up with friends. I’ve lived in the US for six and half years now and while this trip has started to feel routine, it always reminds me of how far the two places I call home really are.

I planned my trip a bit differently this January. When I first moved to the US in 2013, my master plan was to find a job in Silicon Valley, get some experience at a fast growing startup and move back to India to work on an exciting opportunity solving a problem close to my heart. Now if you’re Indian, you’re probably reading this and chuckling. Everybody says this when they first move abroad but very few people actually maintain their conviction. Life happens and all of a sudden, it just doesn’t make sense to move back.

Over the past six and a half years, I’ve flip-flopped between staying in the US and going back. But in 2019, I finally made up my mind. I was moving back. I realized I needed to now figure out how to best position myself for the switch, which had to start with learning more about what’s happening on the ground in India.

I reached out to a lot of people in the Indian tech community to find some answers. Some I knew already and others I found via responses to this tweet and cold DM’ing people I’ve been following and admire.

In India from Jan 4 – 21. Who are some VCs and founders I should talk to? Specifically trying to learn more about what it's like finding quality PMs and operators for early stage cos in 🇮🇳! Will be forever grateful for any introductions 🙌

Everyone was extremely generous with their time and I was flooded with a number of insightful opinions about what’s going on in India.

In this post, I’ve synthesized my learnings from these conversations and added some general observations on how technology is changing everyday life in India. Through these conversations, my goal was to answer four questions –

Where is the market opportunity?

What does the availability of talented people look like?

Why are people moving back to India?

Are there reasons to be cautious?

Bharat is wide, but shallow.

I’m not exactly sure when everyone started talking about Bharat, but it seems to have happened in 2017 when Jio started picking up momentum, demonetization briefly made PayTM the technology darling of India, and UPI usage started growing at double digit rates month over month. I even wrote this piece in Techcrunch trumpeting the same phenomenon. Turns out I was quite wrong – American companies immediately got their act together, with Walmart acquiring Flipkart and as a result PhonePe and Google riding on UPI to dominate payments with Google Pay. India surpassed 300 million smartphone users in 2017 and seemed to be on track to hit more than 800 million by 2022. It was starting to look like a lot of the infrastructure was in place for a new generation of companies focused on serving millions of people that were now coming online for the first time.

The good news in 2020 is that the expansion of digital infrastructure shows no signs of slowing down and internet subscriber numbers are increasing with McKinsey counting 560 million internet subscribers at the end of 2019. India also overtook the US to become the world’s second-largest smartphone market. It’s fairly certain that this decade will end with every single Indian equipped with a smartphone, data that’s almost too cheap to meter, and low-cost digital payments at their fingertips.

The bad news is that Bharat hasn’t turned out to be a homogeneous demographic. As Sajith Pai pointed out this year, India isn’t just two countries — the urban affluent class and the rest of India, but four! And the fact still remains that people in India2 and India3 still do not have disposable incomes large enough to sustain a large number of companies. Just look at Sharechat’s woes.

Everyone I spoke to broadly agreed with this categorization, but I heard different takes on Bharat’s trajectory. They ranged from downright pessimistic — if you want to build for the developing country mass market you’re much better of also focusing on SEA and middle class Africa, to the cautiously optimistic — regardless of how the economy does in the 2020s, startups that create novel business models and products with a high utility to simplicity ratio will have high chances of success.

My take — there might be pockets of opportunity, but there’s unlikely to be a lot of companies serving Bharat with viable business models unless disposable incomes start rising again.

B2B marketplaces and SME focused software is taking off

While the lack of disposable incomes might present an obstacle to B2C companies, the emergent digital infrastructure has made it the best time ever to start a B2B marketplace company. I compiled a list of these startups a couple of months ago. I’ve struggled to keep it up to date, such has been the pace of fundraising and activity in this space.