Peloton went public in September 2019. Since then, barring a blip in March when the entire market sold off, the stock is up 70%. It’s winning big in the quarantine economy as people looking for alternatives to gyms, sports and fitness classes have turned to its slick connected bikes and treadmills and streaming content. You can directly stream live and recorded fitness classes produced by Peloton on screens attached to the bike and treadmill, or you can purchase a standalone digital subscription that gives you access to the same content. Their streaming service is available on all major platforms. The content is always fresh and engaging, with many Peloton instructors becoming social media celebrities over the years.

| Quarter | July – Sept 2019 | Oct – Dec 2019 | Jan – March 2020 |

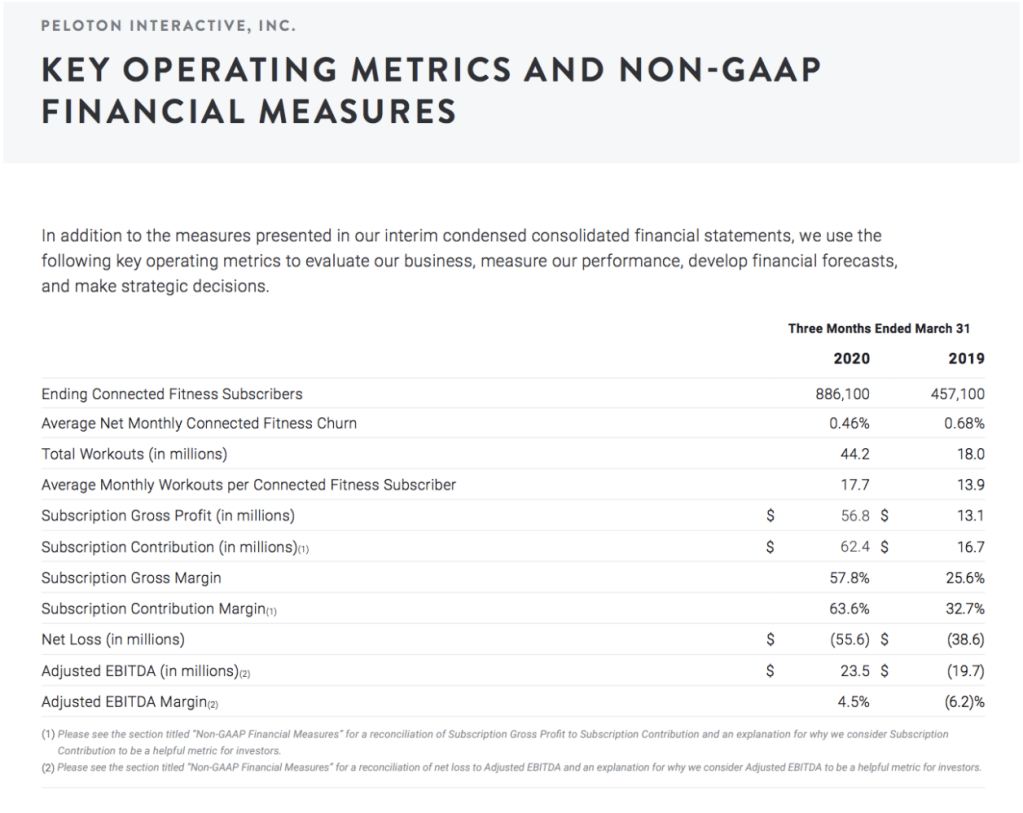

| Revenue (millions) | $228.00 | $466.30 | $524.60 |

| Connected Fitness Product Revenue (millions) | $157.60 | $381.10 | $420.20 |

| Digital Subscription Revenue (millions) | $67.20 | $77.10 | $98.20 |

Most startups are supposed to fail, and this was especially true for Peloton. When CEO and co-founder John Foley was looking for investors after burning through a seed round trying to prove out the concept, he was rejected by both fitness industry insiders and venture capitalists. He even tried to partner with Flywheel, one of the pioneers of the studio cycling craze. From this Inc.com from 2016 –

Meanwhile, Foley approached Flywheel about joining forces. The idea was that Peloton would continue building out its business model, but become part of Flywheel and use its classes as content. The deal fell through. (Zukerman (Flywheel founder) says neither she nor current management was involved in any talks with Peloton. Foley says he dealt with the company’s prior chairman, David Seldin, and former CEO, Jay Galluzzo.)

He decided to go it alone after Flywheel turned him down. Similar discussions with SoulCycle also didn’t go anywhere (they must be kicking themselves right now). Peloton would build the bike hardware and software and create the streaming content from scratch. This new direction for the business made the already challenging task of raising funding for a business without any precedent even harder.

From the same Inc.com profile:

It was true that Foley could offer no research to convince potential investors that a market existed. He was relying on his gut instinct, which told him that there had to be lots of people like him out there who would love to own what he was building. Ironically, more than a few VCs told him, “I’m not going to invest, but when you build this, let me know, because I want to buy one,” he says.”

After a $3.5 million Series A and a relatively underwhelming kickstarter campaign in 2013, Foley realized Peloton needed to get into retail for the concept to take off. His intuition was that early adopters needed to physically experience the bike and streaming classes to be convinced to pull the trigger. They also realized they couldn’t outsource delivering the bike to third-party logistics companies. Assembling and setting up the bike was a critical part of the experience they had to bring in-house to ensure quality.

In its first two years, Peloton had gone from a company trying to build a connected bike and video streaming infrastructure to a retail company with its own logistics arm. But they weren’t done! They still needed cycling classes to stream and SoulCycle and Flywheel refused to partner with them. So Peloton built their own content production operation and started directly hiring instructors.

Today, Peloton is a fully integrated provider of at-home fitness experiences. They manufacture the bikes themselves (having purchased Taiwanese bike manufacturer Tonic in October 2019), deliver the bikes using an in-house logistics team, operate retail stores and live studio sessions in NYC and London, produce high quality fitness videos and operate streaming infrastructure that delivers this content to their bikes and treadmills but also phones, tablets, computers and TVs all over the world.

This has allowed them to build a business with incredible growth and unit economics. Peloton today has two types of customers — ‘Connected Fitness Subscribers’ that purchase the bike or treadmill and a streaming subscription, and ‘Digital Subscribers’ that only purchase the streaming subscription. The former pay $39/month for access to classes and profiles tracking metrics and performance for the entire family, while the latter pay $13/month for individual subscriptions to streaming content only.

[CAC] Hardware gross margins are funding capital-efficient customer acquisition

| Quarter | July – Sept 2019 | Oct – Dec 2019 | Jan – March 2020 |

| Connected Fitness Subscribers | 562,774 | 712,005 | 886,100 |

| Connected Fitness Subscribers YoY Growth | 26.52% | 24.45% | |

| Digital Subscribers | 105,856 | 109,000 | 176,600 |

| Digital Subscribers YoY Growth | 2.97% | 62.02% | |

| Total Subscribers | 668,630 | 821,005 | 1,062,700 |

| Total Subscribers YoY Growth | 22.79% | 29.44% | |

| Connected Fitness Product Gross Margin | 43.00% | 40.50% | 45.30% |

| Connected Fitness CAC (Weighted Average) | $1,293.18 | $1,031.59 | $461.34 |

| Digital FItness CAC (Weighted Average) | $101.75 | $21.73 | $179.14 |

| CAC | $1,394.93 | $1,053.32 | $640.48 |

| GM per incremental connected fitness subscriber | $1,314.05 | $1,034.27 | $1,093.37 |

Peloton is a high CAC business. The bikes and treadmills are expensive and target affluent customers that cost a lot to reach and serve. The digital subscription is more affordable, but the content is designed to appeal more to urban millennials that tend to have more fitness alternatives. It’s also a novel concept, requiring generous promotional offers and perks like 0 APR financing and free delivery and installation services that all roll up into CAC. But high CAC by itself isn’t a problem. It needs to be looked at in the context of the company’s other unit economics.

As Ben Thompson pointed out in his analysis of Peloton’s S-1 (paywall), the gross profit they made on each bike sale more or less made up for the cost of acquiring that customer which means all subscription services revenues, less the cost of producing and delivering that content, went straight to the bottom line!

This has continued to be the case in 3 out of the 4 quarters since the company went public. They don’t directly report a CAC in their 10Q, so I had to estimate it by dividing each quarter’s sales and marketing expense by the new subscribers added in that quarter. They also started disclosing how many subscribers they added for each category only after going public. Since these customers are purchasing fundamentally different products (to start at least), I decided to assign a separate CAC for each category weighted by their total net additions in the quarter. Unfortunately because they didn’t disclose digital subscriber numbers prior to Q1 of the 2019 calendar year year, I could only start comparing weighted average CACs from Q3 2019 onwards.

Looking at the combined CAC for both types of customers, this trend has continued, and seems to be improving. Peloton added ~149k Connected Fitness Subscribers in Q4 2019, bringing in $154m in gross margin dollars and spent $160m on Sales and Marketing. They added ~174k in Q1 2020, bringing in $190m in gross margin dollars and spent $154m on Sales and Marketing. Their ability to continue selling bikes and treadmills is critical to their ability to keep acquiring customers in a capital efficient manner. They recently paused treadmill delivery because of ‘the high touch nature of it’s assembly’. Some skeptics speculate it could also be because treadmills haven’t sold very well. I couldn’t find any definitive information on this though.

[Growth] Content and community are the company’s future

For what’s likely the first time in the company’s history, Digital Subscribers grew faster than Connected Fitness Subscribers in Q1. The pandemic obviously played a huge part in this, and it seems unlikely they’ll see a jump this big in quarter-over-quarter growth rates again, but Peloton’s starting to look more and more like the Netflix of fitness. Foley at least seems to think that the subscription business could be more valuable in the long run. From this Forbes piece before their IPO:

“It’s funny. Internally, I happen to be one of the people in the leadership team to think that [digital subscriptions] could over time eclipse the the core connected fitness business,” Foley says. “We are going to be watering the acorn that is a pure digital business and bringing that to as many people as possible.”

Peloton offers all kinds of live and on-demand fitness classes, which are then curated into collections and challenges.

They’ve built a community of 1 million members around this content. Members can ‘wear tags’ to show their affiliation with physical communities, causes and identities. They earn badges for hitting milestones in different work out categories. While a thorough breakdown of Peloton’s community features and dynamics, both within the app and on social media, is a topic for a separate post, it’s clear Peloton has a massive opportunity here. They have a heavily engaged user base, with average monthly workouts per user trending upwards even as the company adds more customers at a record clip.

Finally, the entire experience would suffer significantly in the absence of great instructors and Peloton seems to have the best. Instructors like Robin Arzon and Alex Toussant have large independent social media followings — 436k and 177k followers on Instagram each. They also have exclusive contracts with the company as far as I can tell, and also get some of their compensation in stock, heavily incentivizing them to help the company succeed. They’re always promoting Peloton when they promote themselves. It’s not that different from professional sports — when Russel Westbrook or Ronaldo post something online, it’s free marketing for the Rockets or Juventus, but also for their sports leagues because there’s only one place you can watch them play. Instructors help Peloton acquire new customers organically and their celebrity status keeps existing customers loyal.

[Subscription Contribution Margin] Strong positive feedback loops

| Quarter | July – Sept 2019 | Oct – Dec 2019 | Jan – March 2020 |

| Subscription Contribution Margin | 63.00% | 64.40% | 63.60% |

| Avg Monthly Workouts per Connected Fitness Subscriber | 11 | 12.6 | 17.7 |

| S&M expenses (millions) | $77.60 | $160.50 | $154.80 |

| Connected Fitness Payback Period (months) | 33.16 | 26.45 | 11.83 |

| Digital Subscriber Payback Period (months) | 12.43 | 2.60 | 21.68 |

| Avg Net Monthly Connected Fitness Churn | 0.90% | 0.74% | 0.46% |

| Connected Fitness Lifetime (months) | 111.11 | 135.14 | 217.39 |

Subscription Contribution Margin is a measure of how much streaming revenues contribute to the bottom line after subtracting the costs of content production.

Peloton’s on a great trajectory here, with an increase of 30% year over year. It’s held steady on a quarter over quarter basis with the company attributing that to expanding to new fitness categories. They expect this to continue being the case for at least the next quarter, guiding to a Subscription Contribution Margin of 63.0% to 64.0% in their most recent shareholder letter. To me, the fact that they expect margins to stay unchanged is a sign that they’re continuing to aggressively invest in fitness content.

Leveraging the fixed costs of content production is key to building a durable moat. When combined with their capital-efficient customer acquisition and low churn, each new Peloton customer gives them additional dollars to invest in customer acquisition and content production. This is a strong positive feedback loop that could allow them to out-execute the competition in the near term.

Peloton’s Moat

Who does Peloton compete with? If you drink the company’s kool aid, they have no real competitors. Peloton is the only fully integrated technology-media-software-product-experience-fitness-design-retail-apparel-logistics company. This image is from their S-1.

But it’s obvious they’re in direct competition with gyms and boutique fitness classes. Anyone skeptical of the company will also note that the at-home fitness industry has been around for decades.

NordicTrack has been around since 1975 and makes treadmills, bikes, ellipticals and strength machines. Their bikes and treadmills are a lot cheaper than Peloton’s – $1999 vs $2245 and $2999 vs $4295 respectively. They also have a streaming service called iFit that comes bundled with the equipment. As far as I can tell, they don’t sell a standalone subscription. Unfortunately NordicTrack is privately held so I couldn’t easily find their operating metrics.

But Nautilus Inc, which makes treadmills, ellipticals, bikes and recumbents, is a public company. Their bikes and treadmills are even cheaper – $699 vs $2245 and $1,399 vs $4295. Notably, Nautilus is just an equipment company — they don’t have a community, instructors or a streaming service. They have slightly lower gross margins than Peloton. From their latest 10-Q:

Gross profit decreased by $0.2 million, or 0.7%, for the first three months of 2020 to $35.6 million, or 38.0% of net sales, compared to gross profit of $35.8 million, or 42.5% of net sales, for the first three months of 2019. The decrease in gross profit dollars was primarily due to lower gross margin percentages in both the Direct and Retail segments. Gross margin percentage points decreased by 4.5% for the first three months of 2020 compared to the first three months of 2019 primarily due to unfavorable sales mix and higher landed product costs.

And then there’s Echelon, a startup based out of Tennessee, that Peloton sued last year for trademark infringement. Their most expensive bike costs $1999.

Given this landscape, I think Peloton’s moat comprises of it’s instructors, community, continuing to leverage content production costs and maintaining hardware gross margins.

Instructors are the most important part of the experience, and by tying them to exclusive contracts Peloton ensures their classes are highly differentiated. Their community can generate strong network effects, and I believe they’ve only scratched the surface here. I won’t be surprised if they go on to challenge a company like Strava, or even acquire them. Continuing to leverage content production and maintaining hardware gross margins is going to be a lot harder. As the at-home fitness market expands post-COVID, it’s quite likely a deep pocketed competitor will enter with a cheaper bike and content that has a similar production value.

For now though, a lot is going in their favor. SoulCycle has been caught completely flat-footed by the pandemic. Delays in delivering their new bike are causing even the most loyal SoulCycle fans to switch:

“I was waiting, waiting, waiting because I wanted the SoulCycle bike to come out. They released the pre-order, and I realized they didn’t service the area that I’m in,” said Erica Baddley, 26, who used to routinely drive 45 minutes from her home to the nearest studio, in Denver. “I would have been first in line.” Four weeks ago, Ms. Baddley ordered a Peloton.”

The same article also estimates that the American fitness club industry lost $3.5 billion in revenue between March 26 and May, which could rise to $6 billion if gyms stay closed through June 1. And even if they do open, there’s no guarantee customers will return.

Looks like Peloton is in the right place at the right time with the best possible product. 2020 is going to be an eventful year for them.

This post is for informational purposes only, you should not construe any such information or other material as investment advice. I may have held positions in Peloton stock at the time of writing.